A patent in India remains valid for 20 years from the filing date, subject to payment of annual renewal fees. If renewal fees are not paid within the prescribed timeline, the patent is treated as having ceased to have effect from the renewal due date.

The law provides a 6 month extension period to regularise delayed payment. If renewal is not completed within that period, restoration under Section 60 becomes necessary.

Many patentees discover cessation only during enforcement, licensing discussions, funding rounds, or due diligence. Administrative oversight, change of patent agents, or internal process gaps are common causes.

Indian law allows restoration within 18 months from the cessation date, but the remedy is discretionary. The Controller must be satisfied that the omission was unintentional and that the request was filed without undue delay.

This article explains the statutory timelines, the difference between late renewal and restoration, and the practical considerations that influence restoration decisions.

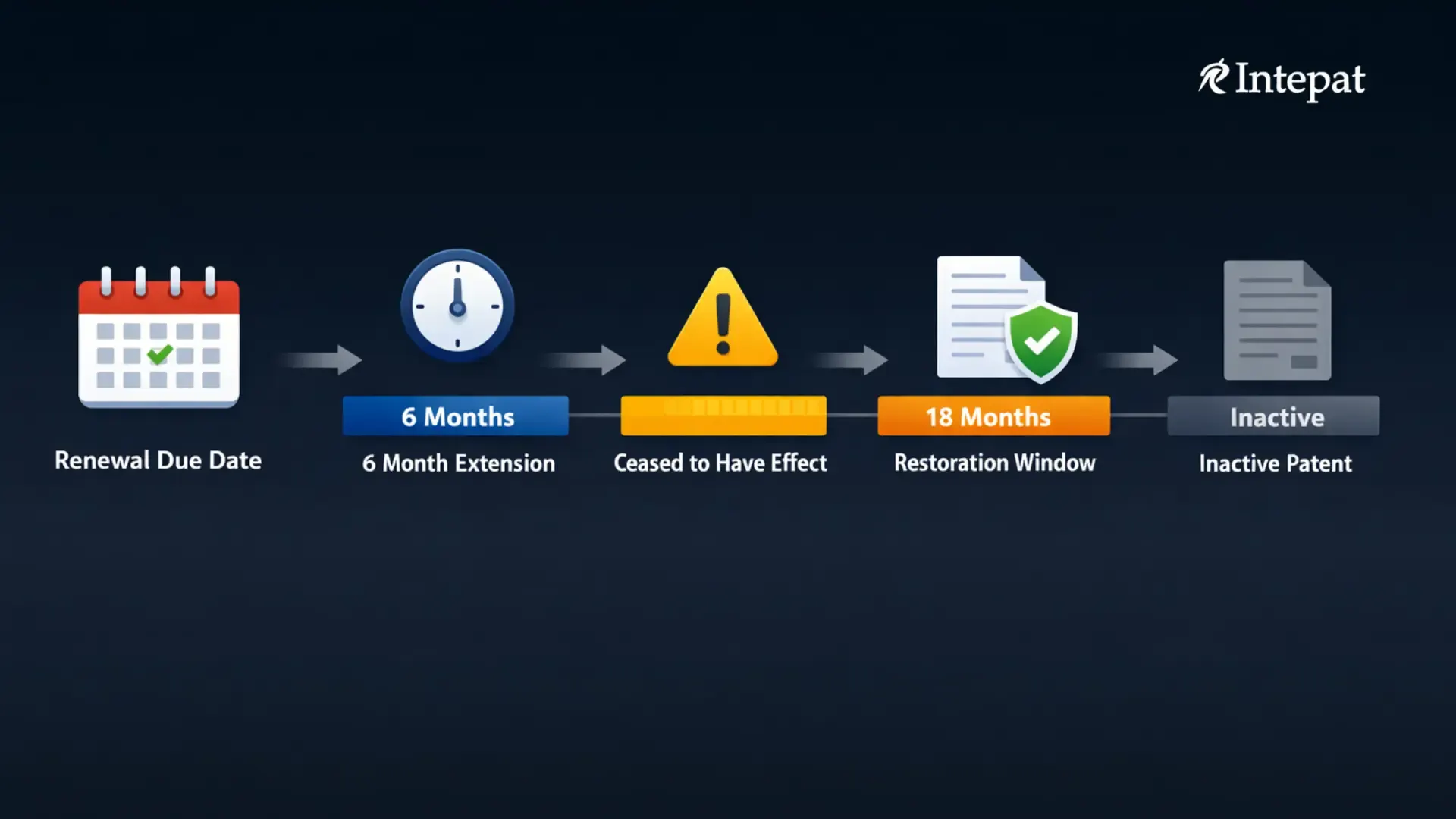

When Does a Patent Cease to Have Effect in India?

A patent does not automatically lose legal status the moment a renewal due date arrives. The law provides a structured sequence before rights are finally treated as ceased.

To understand this properly, break the process into 3 stages.

1. Annual Renewal Obligation

Under the Patents Act, a patentee must pay renewal fees every year to keep the patent in force.

The first renewal becomes payable before expiry of the 2nd year from the date of patent in respect of the 3rd year. Thereafter, renewal fees must be paid before the beginning of each succeeding year.

If renewal fees are not paid within the prescribed time, statutory consequences follow.

2. Six Month Extension Window

If renewal fees are not paid on or before the due date, the Patents Rules allow an additional 6 month period to complete payment.

During this extension period:

- The patentee must file Form 4 requesting extension under Rule 80(1A).

- The prescribed extension fee per month of delay must be paid.

- The renewal fee for the relevant patent year must be paid.

If these steps are completed within the 6 month window, the patent continues in force without the need for restoration.

This extension is procedural. It does not require justification or discretionary approval. It is a statutory opportunity to regularise delayed payment.

3. Cessation of Patent Rights

If renewal fees are not paid even within the 6 month extension period, the patent is treated as having ceased to have effect.

In practice, the Patent Office records the Date of Cessation as the renewal due date where renewal fees remain unpaid. This recorded cessation date becomes critical for calculating restoration timelines.

From the cessation date:

- Exclusive rights are no longer enforceable.

- Third parties may begin commercial use of the invention.

- The 18 month restoration limitation begins to run.

Although the law provides a 6 month extension to regularise payment, where renewal ultimately remains unpaid, cessation relates back to the original renewal due date for record and limitation purposes.

Practical Illustration

To understand how this operates in practice, consider the following example:

Date of Patent: 20 July 2022

Renewal due date for the 3rd year: 20 July 2024

No renewal paid within the permitted period

The Patent Office records the Date of Cessation as 20 July 2024.

The restoration application must therefore be filed within 18 months from 20 July 2024.

Restoration deadline: 20 January 2026.

This reflects how cessation and restoration limitation are recorded in actual Patent Office practice.

Important Distinction

It is essential to distinguish between:

Late renewal within 6 months, and

Restoration after cessation.

Late renewal requires filing Form 4, paying the prescribed extension fee per month of delay, and paying the applicable renewal fee within the 6 month extension window.

Restoration requires filing Form 15 under Section 60 and Rule 84, providing a detailed explanation supported by evidence, paying the restoration fee and outstanding renewal fees, and satisfying the Controller that the omission was unintentional.

Late Renewal Payment Within 6 Months

If the patentee does not pay the renewal fee on or before the renewal due date, the patent lapses from that due date.

However, the Patents Rules provide a statutory 6 month extension period to complete the payment.

During this 6 month window:

- The patent is treated as lapsed.

- The patentee can still regularise the renewal.

- Restoration under Section 60 is not required.

To regularise delayed renewal within this period, the patentee must:

- File Form 4 requesting extension of time under Rule 80(1A).

- Pay the prescribed extension fee for each month or part of a month of delay.

- Pay the renewal fee for the relevant patent year.

The extension fee applies per month of delay.

As per the current First Schedule of the Patents Rules:

For e filing:

- Natural person, startup, small entity, educational institution: ₹480 per month

- Others: ₹2400 per month

For physical filing:

- Natural person, startup, small entity, educational institution: ₹530 per month

- Others: ₹2600 per month

The official fee schedule is available in the First Schedule of the Patents Rules on the website of the Indian Patent Office.

If the patentee completes these steps within 6 months from the renewal due date, the Patent Office records the renewal and the patent continues in force. No explanation for delay is required at this stage.

You can calculate renewal fees and extension charges using our Patent Renewal Fees Calculator, which covers annual renewal and the 6 month extension window.

Restoration of a Patent Under Section 60 and Rule 84

If renewal fees are not paid within the permitted 6 month extension period, the patent ceases to have effect. The Patent Office records the cessation date as the renewal due date where renewal remains unpaid.

Section 60 of the Patents Act read with Rule 84 provides a limited statutory mechanism for seeking restoration of such a patent.

Restoration is not automatic. It is a discretionary remedy.

Limitation Period

A restoration request must be made within 18 months from the date on which the patent ceased to have effect.

In cases of non payment of renewal fees, this limitation period is computed from the recorded cessation date, which corresponds to the renewal due date.

The Controller does not have discretion to extend this 18 month statutory limit.

Nature of the Restoration Request

A restoration request is made in Form 15 and must be supported by a detailed statement explaining the circumstances that resulted in non payment of renewal fees.

The central requirement under Section 60 is that the omission must have been unintentional.

The Controller examines:

- The factual circumstances leading to non payment

- The systems in place to monitor renewals

- The timing of discovery of cessation

- The promptness of corrective action

- Whether third party interests have intervened

The burden lies on the applicant to establish that restoration is justified.

Publication and Opposition

If the Controller forms a prima facie view in favour of restoration, the request is published in the Official Journal.

Third parties may oppose restoration within the prescribed period.

The Controller considers any opposition before making a final decision.

Effect of Restoration

If restoration is allowed and all outstanding fees are paid, the patent regains legal effect.

However, statutory safeguards may protect third parties who commenced use of the invention during the period of cessation.

Failure to Seek Restoration Within Time

If no restoration request is made within 18 months from the cessation date, the patent cannot be revived.

At that stage, the patent permanently ceases to have effect. The rights are extinguished, and the invention falls into the public domain.

From a portfolio management perspective, such a patent is treated as an inactive patent, meaning it no longer confers enforceable exclusivity and cannot be restored under the statutory framework.

If the patent retains strong commercial relevance, restoration should be pursued without delay.

Practical Risks and Strategic Considerations

Restoration under Section 60 provides a statutory remedy, but it does not guarantee revival of rights. The Controller evaluates intent, timing, documentation, and surrounding circumstances before allowing restoration.

Before initiating restoration, patentees should consider 3 critical factors.

1. Strength of the Explanation

Restoration depends fundamentally on whether the failure to pay renewal fees was unintentional.

The Controller may assess:

- The internal systems in place to track renewals

- Whether responsibility was clearly assigned

- Whether the omission resulted from isolated oversight or systemic neglect

- The quality of documentary evidence supporting the explanation

A general assertion of oversight carries limited weight. A structured explanation supported by records materially improves credibility.

2. Timing of Corrective Action

Although the law permits filing within 18 months from the cessation date, delay in taking corrective action can weaken the overall case.

The Controller may consider:

- When the patentee became aware of cessation

- The time taken to initiate restoration proceedings

- Whether there was avoidable delay after discovery

Prompt action reflects diligence. Prolonged inaction after awareness may adversely affect the discretionary assessment.

3. Intervening Third Party Use

Once a patent has ceased to have effect, third parties may begin commercial use of the invention.

If restoration is later granted, statutory safeguards may protect those who commenced use during the period of cessation. This creates commercial uncertainty.

The longer the period between cessation and restoration, the greater the possibility of intervening rights.

Commercial Evaluation Before Restoration

Restoration should not be pursued mechanically. A strategic evaluation is advisable.

Patentees should assess:

- Remaining term of protection

- Current commercial relevance of the invention

- Licensing or enforcement prospects

- Competitive landscape

- Total statutory and professional cost

Where the patent continues to hold commercial significance, restoration should be pursued without delay and supported by structured documentation.

Where commercial value has materially declined, restoration may not be economically justified.

Conclusion

MissMissing a patent renewal deadline does not immediately eliminate all statutory remedies. The law provides a structured framework:

- A 6 month extension period to regularise delayed renewal.

- An 18 month restoration window calculated from the recorded cessation date.

However, restoration is discretionary. The Controller evaluates the nature of the omission, the timing of corrective action, and potential third party impact before allowing revival.

Delay increases procedural risk. Weak documentation reduces credibility. Commercial value should guide the decision.

Where a patent continues to hold strategic or commercial importance, restoration should be approached with clarity, proper documentation, and structured legal assessment. Preventive renewal management remains the most effective safeguard against cessation.

Restore or Secure Your Patent Rights Before It Is Too Late

Unsure about renewal timelines or restoration eligibility? Get a clear assessment of deadlines, fees, and procedural options before rights are permanently affected.

Frequently Asked Questions

1. How long does a patent remain valid in India?

A patent in India remains valid for 20 years from the filing date, subject to payment of annual renewal fees. Failure to pay renewal fees within the prescribed timeline results in the patent ceasing to have effect.

2. What happens if a renewal fee is not paid on the due date?

If renewal fees are not paid on or before the due date, the Patents Rules allow a 6 month extension period to regularise payment by filing Form 4 and paying the prescribed extension fee along with the renewal fee.

If renewal is not completed within that 6 month period, the patent ceases to have effect.

3. From which date is the 18 month restoration period calculated?

The 18 month limitation period is calculated from the date on which the patent ceased to have effect.

In cases of non payment of renewal fees, the Patent Office records the cessation date as the renewal due date, and the restoration period is computed from that date.

4. Is restoration of a patent automatic?

No. Restoration under Section 60 is discretionary. The Controller must be satisfied that the failure to pay renewal fees was unintentional and that there was no undue delay in filing the restoration request.

5. What fees are payable for restoration?

Restoration generally requires payment of:

- The prescribed restoration fee

- All unpaid renewal fees

- Any applicable extension or statutory charges

The exact fee amounts depend on the applicant category and are specified in the First Schedule of the Patents Rules.

6. What happens if no restoration application is filed within 18 months?

If no restoration request is made within 18 months from the cessation date, the patent cannot be revived.

The rights permanently cease and the patent becomes an inactive patent.

7. Can third parties use the invention after cessation?

Once a patent has ceased to have effect, third parties may begin commercial use of the invention.

If restoration is later granted, statutory safeguards may protect those who commenced use during the period of cessation.

8. Should every ceased patent be restored?

Not necessarily. Restoration should be evaluated based on:

- Remaining term of protection

- Commercial relevance

- Competitive landscape

- Cost versus expected value

A structured assessment helps determine whether restoration is commercially justified.