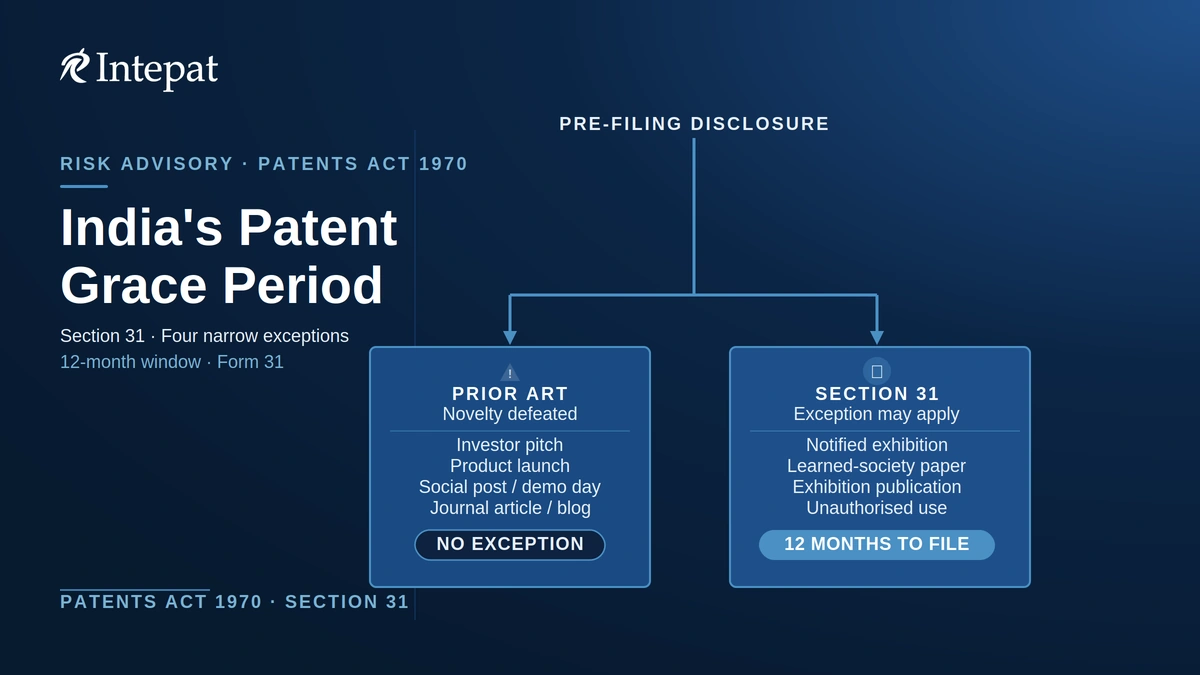

The grace period under Section 31 of the Patents Act, 1970 can let an inventor file within twelve months of certain disclosures without losing novelty. It is narrow. It covers display at a government-notified exhibition, publication arising from that display, unauthorised use during the exhibition, and a paper read before a learned society. It is not a general grace period.

This guide covers Indian patent law, with a brief comparison to other jurisdictions, and is written for founders and inventors deciding whether a disclosure they have already made still leaves room to file.

| Quick answer |

| India has no general grace period. Most non-confidential disclosures before filing, including public pitches, product launches, journal articles, social posts, and sales, can put your own invention into the prior art and defeat novelty. |

| Section 31 covers four narrow situations: display at a government-notified exhibition, publication from that display, unauthorised use during the exhibition, and a paper read before a learned society. |

| The deadline is twelve months from the exhibition’s opening or the paper’s reading or publication, not from any disclosure you happen to make. |

| To claim it, you file Form 31 with evidence, under Rule 29A, in force since 15 March 2024. The e-filing fee is Rs 500 for a natural person, startup, small entity, or educational institution, and Rs 2,500 for other applicants. |

| The safer route is to file a provisional application before you disclose. Section 31 is a fallback, not a plan. |

Does India have a patent grace period?

India does have a grace period, but it is far narrower than many founders assume. The starting rule is strict. Under how Indian patent law defines a “new invention,” the invention must not have been published in any document or used anywhere in the world before you file (Section 2(1)(l)). A single public disclosure before filing can put your own invention into the prior art and defeat your application, because India applies an absolute novelty standard.

Section 31 carves out a small set of exceptions to that rule. If your disclosure fits one of four specific situations, you have twelve months to file without the disclosure counting against you. If it does not fit, the disclosure stands as prior art and the grace period does nothing for you. This is the distinction that catches inventors: a grace period exists, but it does not cover the disclosures that startups commonly make.

Take a common case. A founder demonstrates a working prototype at a public startup demo day, posts a video of it online, and files three months later. Nothing in that sequence fits Section 31, so the demo and the video are prior art against the founder’s own application. The grace period the founder was counting on never applied, and the novelty objection that follows is difficult to answer.

Confidential disclosures are different. Information shared under a non-disclosure agreement or another obligation of confidence does not fall into the public domain, so it generally does not count as prior art. The risk comes from a public disclosure, not from a private, confidential conversation.

The four disclosures Section 31 protects

Section 31 of the Patents Act, 1970 lists four situations where a pre-filing disclosure does not anticipate your invention:

- Display at a notified exhibition. Display or use of the invention, with your consent, at an industrial or other exhibition that the Central Government has notified for this purpose in the Official Gazette.

- Publication from that exhibition. A description of the invention published as a result of the display or use at that exhibition, such as an exhibition catalogue.

- Unauthorised use during the exhibition. Use of the invention by someone else, without your consent, after it was displayed at that exhibition and during the exhibition period.

- A learned-society paper. A description of the invention in a paper you read before a learned society, or published with your consent in the transactions of that society.

All four share the same clock: you must file within twelve months (Section 31). The window runs from the opening of the exhibition or the reading or publication of the paper, not from the day you happened to disclose.

The learned-society limb is read narrowly. The terms “learned society” and “transactions” are not defined in the Act, and they are usually taken to mean the published proceedings of a recognised, non-commercial society. A general journal article, an ordinary conference paper, a preprint upload, or a company blog post should not be assumed to qualify unless it can be tied to a paper read before a learned society or published in the transactions of such a society.

Does a demo day, pitch, or product launch qualify?

The four categories are narrow, so for most everyday disclosures the honest answer is no. The table below maps the disclosures founders ask about most often to whether Section 31 is likely to help.

| Disclosure before filing | Section 31 likely to apply? | Practical note |

| Display at a Central Government notified exhibition, with your consent | Yes, if you file within 12 months | Keep the gazette notification and proof of the exhibition dates |

| Publication in an exhibition catalogue from that display | Yes, if it arose from the notified-exhibition display | Show the publication came from the display |

| Public demo day or startup pitch | Usually no | Unless it was a notified exhibition, or the disclosure was genuinely confidential |

| Product launch, sale, website post, or social media video | Usually no | Treat as risky prior art |

| Paper read before a learned society or in its transactions | Possibly | Keep the society records and publication details |

| Ordinary journal article, preprint, or company blog | Usually no | Do not assume Section 31 protection |

The notified-exhibition requirement inventors overlook

The first three situations only work if the exhibition is one the Central Government has specifically extended Section 31 to, by notification in the Official Gazette (Section 31(a)). A trade show, a demo day, or a startup expo is not automatically covered. Before you rely on an exhibition disclosure, you need to confirm that a notification exists for that exhibition. If there is no notification, the display is an ordinary public disclosure and it can destroy novelty like any other.

This is the practical trap. Founders read “display at an exhibition is protected” and assume any exhibition counts. It does not. The protection is tied to the gazette notification, and the burden is on you to show that the notification exists.

Section 31 versus the other anticipation exceptions

Section 31 is often described loosely as a “one-year grace period,” which blurs two separate provisions. Section 31 gives twelve months for the exhibition and learned-society situations above. Section 32 is a different provision: it protects public working of the invention in India within one year before your priority date (the date your novelty is measured from), but only where the working was for reasonable trial and it was reasonably necessary to work it in public (Section 32). These are the main anticipation exceptions a pre-filing disclosure can fall under.

Two practical points follow. First, neither provision covers an ordinary commercial launch, a sale, or a marketing disclosure, because those are not reasonable trial and they are not notified-exhibition displays. Second, the windows are measured differently: Section 31 runs from the exhibition or the paper, while Section 32 runs from the priority date. If you are counting on either, count from the right event.

Two further exceptions sit alongside these. Section 29 can help where someone published your invention using matter obtained from you, without your consent, provided you did not delay filing once you learned of it. Section 30 covers a disclosure made to the Government for the purpose of investigating the invention. Both are narrow, and neither rescues a disclosure you chose to make yourself. They matter mainly when an idea leaks rather than when you publish it.

A brief comparison helps here. Some jurisdictions, including the United States, give inventors a broad twelve-month grace period for their own pre-filing disclosures. India’s grace period is narrower. The headline number is similar, but India limits it to the four Section 31 categories rather than to disclosures generally. Do not assume that because a disclosure would be forgiven elsewhere, it is forgiven in India.

How to claim it: Form 31, evidence, and fees

Until 2024, the Act provided the grace period but the Rules were silent on how to claim it. The Patents (Amendment) Rules 2024, in force from 15 March 2024, added Rule 29A and a dedicated form. To avail the period under Section 31, you file Form 31 with the prescribed fee (Rule 29A). Form 31 asks for the earliest date of use, publication, or disclosure of the claimed invention, and documentary evidence of the ground you are relying on, such as the gazette notification for the exhibition, proof of your consent, or the record of the learned-society paper.

Form 31 fee (verified June 2026)

| Applicant | E-filing | Physical filing |

| Natural person, startup, small entity, or educational institution | Rs 500 | Rs 550 |

| Other applicants | Rs 2,500 | Rs 2,750 |

Physical filing carries a 10% surcharge (First Schedule, Patents Rules 2003). One boundary is worth stating plainly: this fee is for the grace-period request only. It is separate from, and additional to, your filing fee and your request-for-examination fee, which follow the normal schedule. The Form 31 fee does not file your patent; it preserves your novelty argument for a disclosure that has already happened.

The burden of proof sits with you. The Controller can examine the evidence, and a thin record, with no notification, no proof of consent, or an academic paper that is not in a society’s transactions, can sink the claim even where the timing is right. In practice, Form 31 is filed in relation to the application that relies on it. If the grace-period claim fails, the application does not automatically fall; it may still proceed if the claims can be distinguished from what was disclosed.

What to do if you have already disclosed your invention

If you have not disclosed yet, the answer is simple: file first. Filing a provisional patent application secures your priority date at lower cost and removes the need to rely on Section 31 at all. Filing before any public disclosure is the only route that does not depend on fitting a narrow exception.

If you have already disclosed, work through three questions in order:

- Does the disclosure fit one of the four Section 31 situations? If it was an investor pitch, a product launch, a press article, a social post, or a sale, it almost certainly does not, and the grace period will not help.

- If it fits, are you inside twelve months of the exhibition opening or the paper? If the window has passed, the option is gone.

- Can you prove it? Gather the gazette notification, consent records, exhibition dates, and publication details before you file, because Form 31 requires them.

The order matters. Checking the category before the clock saves you from assembling evidence for a disclosure that was never eligible, and checking the clock before the evidence saves you from preparing a Form 31 you can no longer use.

Where the disclosure does not fit Section 31 or Section 32, it is prior art, and you should get a patentability assessment before spending on a filing that may already be anticipated. A registered patent agent can tell you quickly whether anything patentable survives, and which type of application fits your position.

Frequently asked questions

The grace period under Section 31 of the Patents Act, 1970 is a twelve-month window to file a patent application after specific disclosures without losing novelty. It covers display at a government-notified exhibition, publication from that display, unauthorised use during the exhibition, and a paper read before a learned society.

India has a narrow grace period, not a general one. Section 31 gives twelve months for notified-exhibition and learned-society disclosures. Section 32 gives one year for public working done for reasonable trial in India. Ordinary disclosures, such as launches, sales, and journal articles, are not covered and defeat novelty.

Sometimes, but only if the disclosure fits Section 31 or Section 32 and you file within the time limit. Most public pre-filing disclosures, including launches, sales, and social posts, are not covered and generally destroy novelty under Section 2(1)(l). The safer route is to file before disclosing.

You file Form 31 with the prescribed fee and supporting evidence, under Rule 29A of the Patents Rules 2003, in force since 15 March 2024. Form 31 requires the earliest disclosure date and documentary proof of the ground, such as the gazette notification, consent records, or the learned-society paper.

The Form 31 fee is Rs 500 for a natural person, startup, small entity, or educational institution filing electronically, and Rs 2,500 for other applicants, with a 10% surcharge for physical filing (verified June 2026). This fee covers only the grace-period request, not your patent filing or examination fees.

Usually not. The learned-society limb protects a paper read before a learned society or published in its transactions, which is read narrowly as the proceedings of a recognised, non-commercial society. A general journal article, a conference proceeding, a preprint, or a company blog post is unlikely to qualify.

A disclosure made under a non-disclosure agreement or another obligation of confidence is not a public disclosure, so it generally does not become prior art against your own application. An NDA does not replace filing, though. Before any public pitch, demo, sale, or launch, file at least a provisional application.

Usually not. Section 31 covers exhibitions the Central Government has notified in the Official Gazette, not public events in general. If a demo day was not a notified exhibition and the disclosure was public, it can stand as prior art against your later application. A confidential demo is treated differently.

This article explains the law on the patent grace period under Section 31 in India as at June 2026 and is for general information only. It is not legal advice. Government fees, forms, and procedures change; confirm current figures with the Indian Patent Office before you file. For advice on your specific invention, consult a registered patent agent. Deadlines in this area are strict, and missing the twelve-month window means losing the grace-period option. The figures and timelines here are indicative and may change; do not rely on them for a specific filing without confirming the current position and, where the stakes warrant it, taking professional advice.