The Patent Cooperation Treaty (PCT) lets an Indian startup keep open the option of seeking patent protection across PCT contracting states for up to 30 or 31 months from the priority date, through one international application. Whether that flexibility earns its cost turns on three things: where the customers and competitors sit, when the next funding round closes, and whose name the application is filed under. The third question quietly switches a 90% WIPO fee reduction in or out, and that is the part most founders miss. This guide covers the decision, the real rupee math, and the filing route for a PCT for Indian startups.

What PCT actually gives a startup, and what it does not

PCT does four useful things for a startup. A single international application is treated as a regular national filing in every contracting state on the international filing date, preserving the priority date globally. The applicant receives an International Search Report (ISR) and a non-binding Written Opinion on patentability before national-phase money is committed. (“National phase” means the later stage where the startup picks specific countries and makes a separate filing and payment before each national or regional patent office.) International publication at around 18 months puts the disclosure into the worldwide prior-art base, where it is available as a novelty-defeating reference under the rules of each national patent office. And the decision on which countries to enter is pushed back to 30 or 31 months from priority.

PCT does not grant a worldwide patent. Each contracting state still grants its own patent through its own national phase, applying its own law; the ISR and Written Opinion are not binding on any national office. National fees in each country are deferred, not waived; they arrive at month 30 or 31 in full. And PCT covers only its contracting states, so for non-member countries, Paris or direct filing remains the only path. The fuller picture is in our PCT route from India guide.

The first decision: Paris route, PCT, or India-only

If the whole market is India, none of this applies: a startup files in India only and stops there. The choice below is for startups that may go abroad, and it comes down to the Paris route versus PCT.

| Dimension | Paris route | PCT route |

| When the abroad decision must be made | Within 12 months of Indian priority | Within 30 or 31 months of priority |

| Cash needed at month 12 | Full national filing fees in every target country | One PCT international filing fee |

| Countries kept open | Only the chosen countries | All 158 contracting states, on standby |

| Strong fit when | Two or three target countries are already locked and budgeted | Country list, or budget, is not yet locked |

For most pre-Series A startups the country list is not locked at month 12, because the customer geography is not locked either. PCT exists for exactly that situation. The Paris route is the better fit when two or three target countries are already on the roadmap and the cash is ready.

When PCT pays off, and when it does not

Five questions worth answering before committing. Each is a signal, not a verdict; read them together.

Is a funding round on the runway in the next 18 to 30 months? PCT shifts the largest patent costs from month 12 to month 30 or 31. A startup expecting to close a round inside that window will have cash when the bill arrives; one that does not should price that bill today and ask whether the budget can carry it.

Where are the customers and competitors? PCT earns its premium when the target geography is genuinely uncertain. If the realistic foreign market is one country with one identifiable competitor already there, the Paris route is usually cheaper.

Is the invention software-only, or strongly software-led? Software inventions face Section 3(k) of the Patents Act in India and parallel exclusions elsewhere. The ISR and Written Opinion give an early read before national-phase money is committed. For software that reads like a method of doing business, no filing route rescues patentability; that conversation belongs before any spend.

Has an Indian application been filed yet? PCT can follow an Indian application or be the first filing. The two paths carry different Section 39 requirements, covered below.

Can the startup fund national-phase entries 30 or 31 months from now? The question most often skipped. PCT defers, it does not eliminate. If month 31 will not have funds for the planned countries, PCT is borrowing time the budget cannot repay.

The cost math, in real rupees

The headline cost of a PCT application from India breaks into four pieces: IPO fees on the corresponding Indian filing and on examination, IPO fees for acting as receiving office and search authority, the WIPO international filing fee, and Indian agent fees. The first three are statutory and verifiable. All figures below are verified as of 29 May 2026 against the Patents Rules 2003 (First and Fifth Schedules) and the WIPO PCT Applicant’s Guide, India national chapter.

One practical point first, because it surprises most founders. The WIPO international filing fee is set in Swiss francs and quoted in USD, but RO/IN bills it in rupees at its own administrative rate, not the day’s spot rate. That rate is fixed fortnightly and has recently run around ₹98 to the dollar, above spot, with a small per-USD buffer against currency movement before the money reaches WIPO and a flat charge (Rs 350 up to USD 2,000, Rs 500 above). The rupee demand is therefore higher than a spot-rate calculation suggests, and it is the figure that must be paid by the date in the letter.

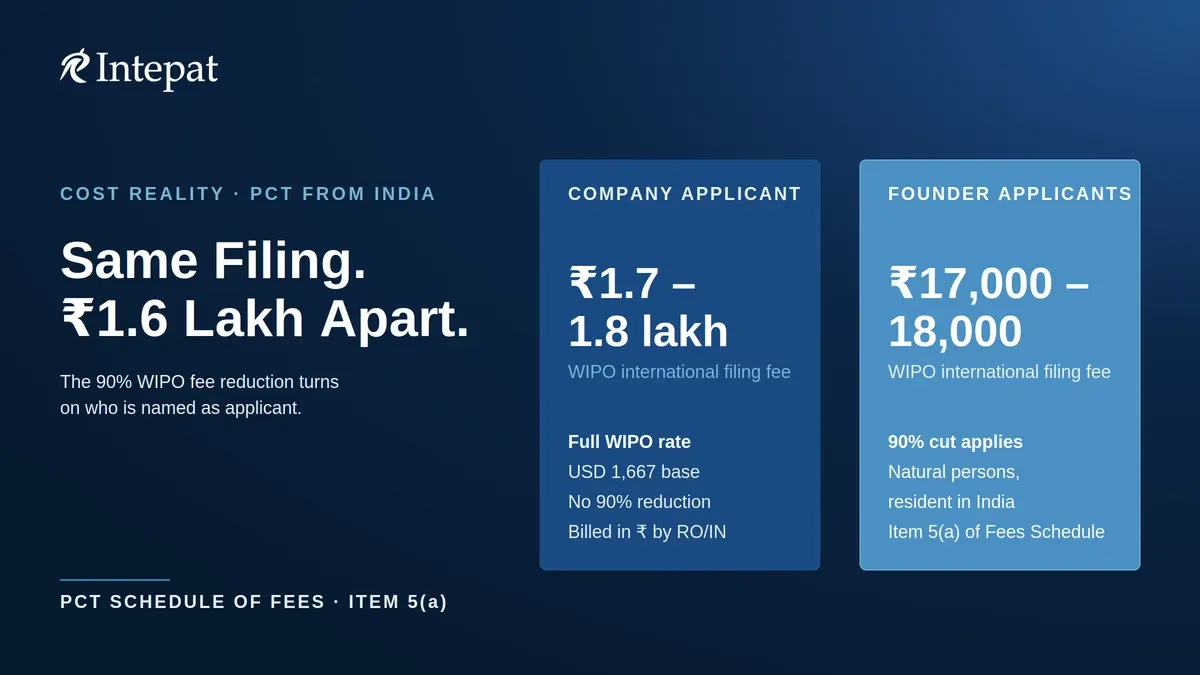

The filing-stage cost then turns on one choice: whether the startup company is the applicant, or the inventor founders are. The company applicant pays the WIPO fee at full rate; founders filing as natural persons get it cut by 90% under item 5(a) of the PCT Schedule of Fees. Both get the ₹2,500 search fee through startup status. The comparison, verified as of 29 May 2026:

| Cost item, at filing stage | Startup company as applicant | Founders as natural-person applicants |

| Indian application fee (e-filing) | ₹1,600 | ₹1,600 |

| IPO search fee, IPO as ISA (Fifth Schedule entry 1) | ₹2,500 | ₹2,500 |

| Transmittal fee (e-filing) | Nil | Nil |

| WIPO international filing fee | Full rate, approx. ₹1.7 to 1.8 lakh | After 90% cut, approx. ₹17,000 to 18,000 |

| Filing-stage out-of-pocket (before agent fees) | Approx. ₹1.75 to 1.85 lakh | Approx. ₹21,000 to 22,000 |

| Request for Examination (falls due later, by month 31) | ₹4,000 | ₹4,000 |

The WIPO fee starts at USD 1,667, rises with page count (USD 19 per sheet over 30), and can be cut by up to USD 376 for fully character-coded e-filing; the 90% reduction, where available, is applied after that. The rupee figures above reflect RO/IN’s administrative conversion described above, not a spot-rate sum. The Request for Examination sits below the filing-stage subtotal deliberately: it is not paid at PCT filing.

The delta and the trade-off. On the WIPO fee alone, the natural-person route saves on the order of ₹1.6 lakh per application: the 90% cut turns a roughly ₹1.7 to 1.8 lakh demand into about ₹17,000 to 18,000. The search fee is ₹2,500 either way. The trade-off is the assignment. The founders hold the rights until they assign to the company, so the assignment must be in writing satisfying Section 68 of the Patents Act, with title recorded under Section 69 read with Rule 90 (Form 16). Investors expect a clean title chain from inventor to entity, settled before filing, not patched during diligence.

A point the fee tables do not state plainly: the two reductions are separate entitlements, and neither is applied automatically. The 90% WIPO reduction depends on who is named as applicant and is claimed in the PCT request; the ₹2,500 search-fee rate is claimed through the e-filing channel with the startup recognition certificate. A company applicant that does nothing will be billed the full WIPO fee and, if it omits the startup claim, the ₹10,000 search fee. Each reduction the filer is entitled to has to be actively claimed at filing.

The second-order cost. These figures cover only the international phase. National-phase entry at month 31 is where the real spend lands: each country adds a national filing fee, translations where required, local agent fees, and over time examination and grant fees. A working estimate is ₹5 to 15 lakh per country across the full lifecycle, varying with jurisdiction. The breakdown is in our PCT entry fee guide for India.

Qualifying for the reductions, and the natural-person filing strategy

Three reductions stack for a startup, and each has to be claimed, not assumed.

Startup fee scale at the IPO. To pay the natural-person (startup) rate on the Indian fees, the entity needs DPIIT startup recognition, and Form 28 is filed with each payment to claim it.

Reduced ISA search fee. When IPO is the International Searching Authority, startup status drops the search fee from ₹10,000 to ₹2,500. It is claimed through the e-filing channel with the recognition certificate; it is not applied automatically.

The 90% WIPO reduction. This one turns on who is named as applicant. Founders filing as natural persons get it; the company does not, and naming the company alongside the founders generally forfeits it. The route is to name the inventor founders as the PCT applicants, then have the company take assignment by a deed satisfying Section 68 of the Patents Act, with title recorded under Section 69 read with Rule 90 (Form 16).

Before using the founder route, check it is actually available. It should not be applied mechanically. Where a founder is already bound by an employment or IP-assignment clause to assign inventions to the company, the rights may already sit with the company, so naming the founder as a personal applicant may be neither accurate nor open. Check it against the founder and shareholder agreements and any board approval needed, settle the assignment before filing, and structure it to both preserve the applicant status the reduction relies on and leave a clean title chain for investor diligence.

How Indian startups file PCT, in eight steps

The working sequence for filing PCT from India. The deeper walkthrough is in our PCT filing guide.

- Decide who the applicants will be. Founders as natural persons qualify for the 90% WIPO reduction; the company does not. If the founder route is chosen, prepare the assignment in parallel.

- File the corresponding Indian application (provisional or complete) at the IPO. This anchors the priority date.

- Choose RO/IN (Indian Patent Office) or RO/IB (WIPO International Bureau). RO/IN is the default for most; RO/IB can simplify multi-applicant or multilingual cases.

- Clear Section 39: wait six weeks after the Indian filing with no secrecy direction, or obtain a Form 25 permit in advance.

- Choose the International Searching Authority (IPO, EPO, AT, AU, CN, JP, SE, or US). Each differs on fee, language, and search quality; the IPO ISA carries the reduced ₹2,500 fee.

- E-file the PCT request with the specification, claims, abstract, and drawings. E-filing claims the up-to-USD 376 reduction under Schedule of Fees item 4.

- Pay the international filing fee, search fee, and transmittal fee (if any) within one month of the international filing date.

- Receive the ISR and Written Opinion at around month 16 to 18, then decide whether to amend under Article 19, file a Chapter II Demand, or hold until national-phase entry.

A pre-flight check covers Form 28, the assignment deed (where applicants are natural persons), the Section 39 permit or six-week confirmation, the inventor declaration, and priority-document availability through WIPO DAS.

What the 31-month wall really means for cash planning

India’s national-phase deadline is 31 months from the priority date, set by Rule 20(4)(i) of the Patents Rules 2003. Most other PCT contracting states use 30 months. Missing the deadline in a target country extinguishes the right to enter that country for that invention, and India is strict: the WIPO India national chapter records that India does not permit reinstatement of rights under PCT Rule 49.6, and the Rule 138 extension of time does not apply to the filing of a national-phase application. Some other jurisdictions allow reinstatement or restoration after a missed deadline, but India should be planned on the basis that no such relief is available.

The wall reads as more time, and that framing is what catches startups. Two reframes help. First, 30 or 31 months is a budget runway, not a thinking buffer: the countries for national-phase entry must be funded by then, each entry being its own filing event with its own forms, translations, and local counsel. The common trap is PCT filed at month 12 to keep options open, then a flat budget at month 30 forcing a single-country entry, so the optionality paid for goes unused. Second, the ISR and Written Opinion at month 16 to 18 are an early read on whether national phase is worth funding: a negative opinion does not bar entry, but it changes the conversation with the next investor.

A founder-friendly view of the timeline:

- Month 0: Indian provisional or complete filed, or Form 25 obtained if filing abroad first

- Month 12: PCT filing deadline, measured from the first (priority) filing

- Month 16 to 18: ISR and Written Opinion expected

- Month 30 or 31: national-phase decisions and the major spend

The background on missed-deadline practice is in our late national-phase entry guide, but for planning, treat the 31-month India deadline as fixed.

Frequently asked questions

No. PCT is a single international application that defers, by up to 30 or 31 months, the decision to file in individual contracting states. Each state still grants its own patent through its own national phase, examined under its own law. PCT defers timing and consolidates paperwork; it does not create a global right.

Not on the WIPO international filing fee, the supplementary search handling fee, or the Chapter II handling fee. Item 5(a) of the PCT Schedule of Fees restricts the 90% reduction to natural persons who are nationals of, and resident in, a qualifying state. A company applicant, however small or recently incorporated, is not a natural person and does not qualify. The Indian fee reductions (IPO application fee, examination fee, IPO-as-ISA search fee) remain available to a recognised startup company on Form 28.

Yes, as long as the entity continues to satisfy the Startup India recognition criteria notified by DPIIT, the natural-person fee scale applies. The Explanation to Rule 7 confirms that if recognition lapses after filing, no difference becomes payable on the original application. The Form 28 status declaration is required at each fee event.

Either path is allowed under Section 39, but the paperwork differs. Path one: file in India first, wait six weeks without any secrecy direction, then file PCT at RO/IN or RO/IB without separate Section 39 permission. Path two: obtain a written permit on Form 25 from the Controller before any PCT filing, used when the six-week period cannot be observed or when there is no Indian priority application. Direct filing at RO/IB needs Form 25 permission unless the six-week clear period has been observed. Getting this wrong is costly: the Indian application can be deemed abandoned under Section 40, any patent granted is open to revocation under Section 64, and Section 118 carries a penalty of up to two years, a fine, or both. When timing is tight, the Form 25 permit is the safe course.

In practical terms, the Indian national-phase right is lost for that PCT application. Rule 20(4)(i) sets the limit at 31 months from priority, and the WIPO India national chapter records that India does not permit reinstatement of rights under PCT Rule 49.6. Any exceptional-relief theory should be treated as litigation-grade and uncertain, not as a filing option. For planning, treat 31 months as a hard deadline. The background is in our late national-phase entry guide.

USD 1,667 is the base international filing fee under PCT Schedule of Fees item 1, plus USD 19 per sheet over 30, so the actual figure rises with page count. Two reductions can apply: an e-filing reduction of up to USD 376 under item 4 for fully character-coded filing, and the 90% reduction under item 5 for qualifying natural-person applicants. Note also that RO/IN bills this fee in rupees at its own fortnightly administrative rate (recently around ₹98 to the dollar) plus a per-USD buffer and a flat charge, so the rupee demand is higher than a spot-rate calculation. The WIPO PCT Applicant’s Guide, India national chapter carries the current figures.

Disclaimer

This article is a practitioner overview, current as of 29 May 2026, with fees, deadlines, and statutory points verified against the Patents Act 1970, the Patents Rules 2003 (First and Fifth Schedules), the PCT Schedule of Fees, the WIPO PCT Applicant’s Guide India national chapter, and the Manual of Patent Office Practice and Procedure. Fee amounts, exchange rates, and scheme statuses change; verify against these primary sources, or contact a patent agent, before acting. Nothing here is legal advice for any specific application.

Related guides

For deeper coverage of the PCT route from India for startups, the following guides in the cluster are written for the same audience:

- The PCT route from India: a complete guide

- How to file a PCT application from India

- PCT entry fees in India, broken down

- Missed the 12-month PCT deadline: what now

- India as ISA for PCT applications

- What every Indian startup should know before filing a patent

- Paris Convention vs PCT: pros and cons

External reference: WIPO PCT Applicant’s Guide, India national chapter